by AdvisorAnalyst.com in collaboration with Franklin Templeton Investments

Bridging the Gap Between Safety and Return

How Franklin Templeton’s Brian Calder is Redefining Cash Management

The Cash Conundrum

For many investors, 2025 has felt like a test of patience and conviction. Cash feels safe—but safety has a cost. In a world where “higher for longer” interest rate expectations meet volatile bond markets and stretched equity valuations, portfolios heavy in cash are quietly underperforming.

“It’s a paradox,” notes Pierre Daillie in AdvisorAnalyst’s in-depth conversation with Brian Calder, Vice President, Portfolio Manager and Senior Bond Trader at Franklin Templeton Fixed Income, for this article. “On one hand, cash feels prudent—dry powder. On the other, sitting idle in a checking account that earns next to nothing, or in a sweep vehicle, which at best, earns a negative real return—that erodes purchasing power.”

Calder, who co-manages the Franklin Canadian Ultra-Short Term Bond Fund (and it's ETF series FHIS) alongside the firm’s other flagship fixed income mandates, has spent more than two decades navigating precisely this intersection—where liquidity meets opportunity. His perspective reflects both the trader’s instinct and the portfolio manager’s discipline: “After years of near-zero rates, investors are rediscovering that cash can actually work again,” he says. “The question is how to make it work efficiently—without losing the security and flexibility investors value most.”

From Idle Cash to Active Strategy

The behavioural shift, Calder observes, has been gradual but clear. “Investors have become more sophisticated and more aware of the drag that cash can apply to portfolios,” he explains. “They want to make sure that every dollar contributes to the overall return, without giving up safety or liquidity.”

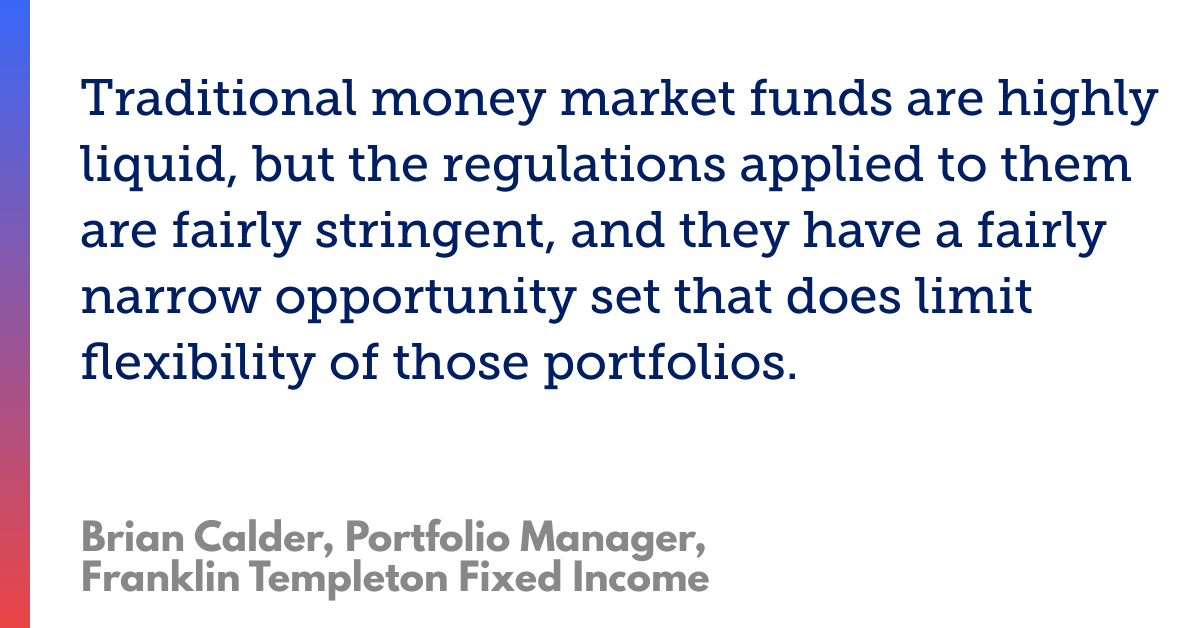

The old toolkit—GICs, high-interest savings accounts, and money market funds—no longer satisfies that balance. GICs lock up capital and penalize early withdrawals; savings accounts have seen yields trimmed by regulatory changes; and money market funds, though highly liquid, are constrained by rules that limit both term and credit exposure.

“The result,” says Calder, “is a narrow opportunity set. Money market products are bound to the very short end of the curve—30, 60, 90-day paper. That limits their flexibility and their yield. Ultra-short bond strategies, by contrast, give you the freedom to move slightly further out the curve, to capture opportunities while keeping rate exposure very low.”

Why is it time to rethink positioning of short term liquid assets?

What's your approach and view to ultra-short bond investing?

Why 'cash' positions should be considered a contributor to total return.

How does scale, depth of research, and active management provide an edge?

How can the ultra-short bond strategy bridge transitions to longer-term investment decisions?

How do the various cash equivalents compare to ultra-short strategies?

What “Ultra-Short” Really Means

Ultra-short bond strategies like FHIS occupy a unique niche—sitting between the traditional money market and short-term bond categories. Calder describes it as “the part of the curve that offers the greatest flexibility.”

“Ultra-short strategies typically operate within a window of about two-thirds to three-quarters of a year in duration,” he explains. “That’s been the sweet spot for us—long enough to earn a meaningful yield, short enough to avoid excessive volatility. Investors don’t want a roller coaster.”

The approach is designed to seize opportunities that are “a little too long” for money market mandates, yet “far less volatile” than conventional short-term bonds. That middle ground, Calder explains, “fills the gap in the fixed income spectrum—helping portfolios stay productive while maintaining liquidity.”

The Active Edge

What sets FHIS apart isn’t just its position on the curve—it’s how actively it’s managed. Calder’s team leverages the scale and depth of Franklin Templeton’s global fixed income platform, executing trades daily across dozens of issuers.

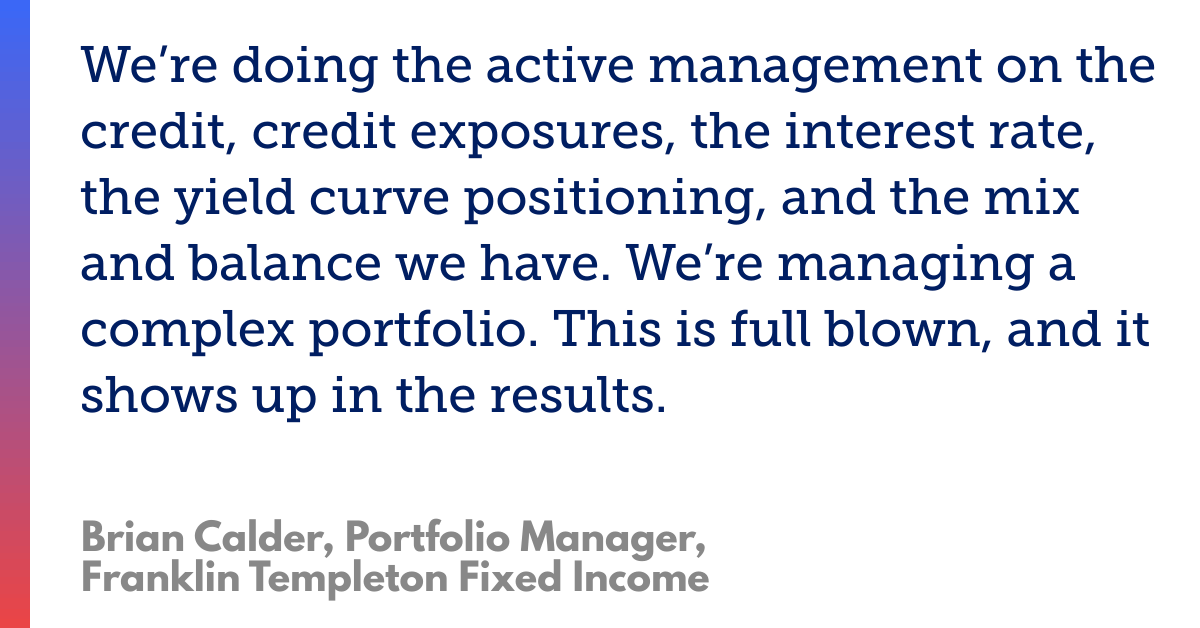

“The bond market is an over-the-counter market,” Calder explains. “It’s not as visible to the retail investor, and efficiency depends on scale. We’re building portfolios of over a hundred positions, benefiting from institutional pricing that’s simply not accessible to individual investors.”

Equally important is the credit work behind those trades. “We rely heavily on our in-house credit analysts,” he says. “They know these companies inside and out. The last place I want to learn about something is in a rating agency report,” he emphasizes. “By then it’s too late. Our goal is to identify opportunities before they hit the public radar.”

That combination of proximity to the market and proprietary research gives FHIS an agility most passive vehicles lack. “It’s not a simple T-bill fund,” Calder emphasizes. “We’re managing exposure to corporates, government paper, even a modest high-yield allocation—all within a disciplined framework. The complexity shows up in the results.”

Built for All Seasons

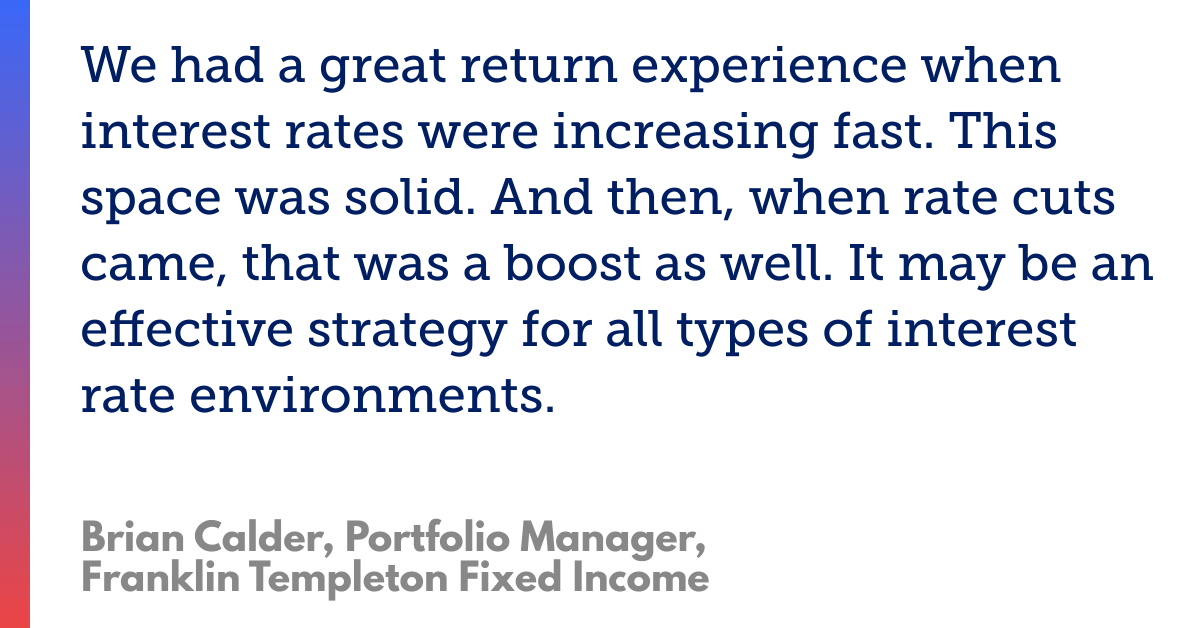

One of the strategy’s under-appreciated strengths is its resilience across rate cycles. “When we launched FHIS, policy rates were still near zero,” Calder recalls. “People wondered why anyone would care. But when rates started rising, the strategy performed exceptionally well. And now, as rates begin to ease, it’s benefitting again.”

That resilience comes from its focus on the “front end of the curve”—the zone least sensitive to large rate swings. Calder puts it simply: “We’ve seen great returns when rates were rising rapidly, and now we’re seeing another tailwind as they come down.”

Real Yield, Real Flexibility

FHIS is designed to function as a strategic fixed income holding—pursuing higher yields with minimal volatility. For some advisors, it’s used as a volatility reducer, paired with longer-duration bond funds to smooth portfolio performance.

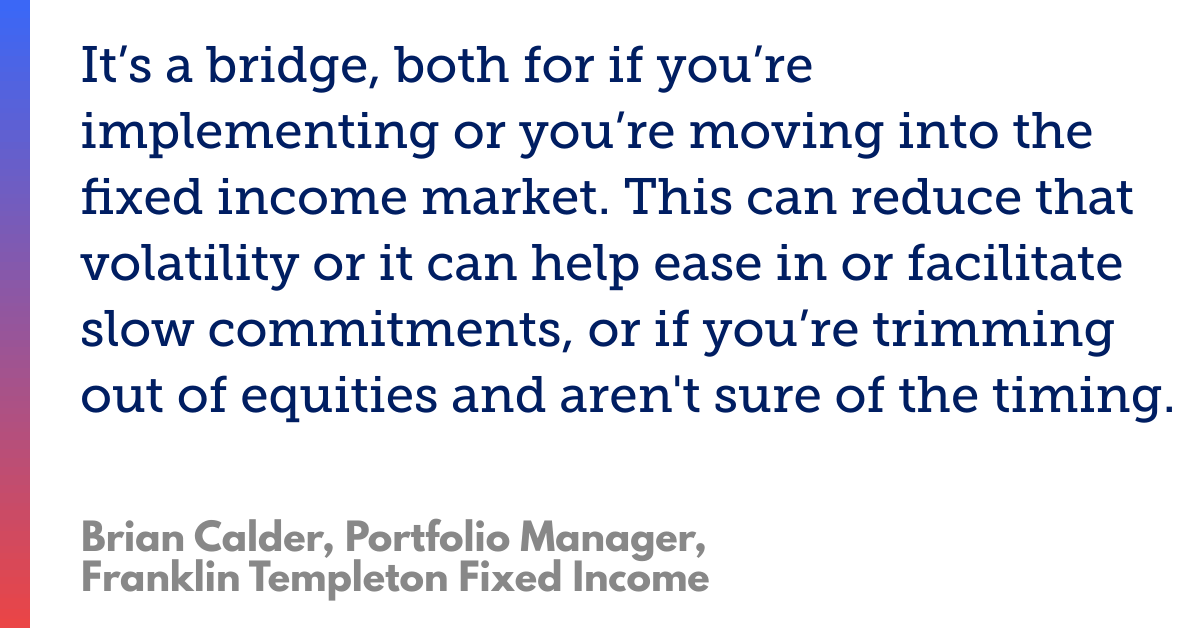

“It works beautifully as a transition vehicle,” Calder notes. “If you’re trimming equities but not ready to commit to longer-term bonds, FHIS lets you stay invested, pursue a healthy yield, and retain daily liquidity. And if you’re managing withdrawals or de-risking a portfolio, it lets you shorten duration without giving up income.”

The fund’s duration target of less than a year and its daily liquidity make it an adaptable building block. “It reduces cash drag,” Calder says. “You’re putting your liquidity to work while maintaining access. That’s exactly what investors want in uncertain times.”

Making Cash Count

To Calder, the conversation about cash is ultimately about opportunity cost. “Holding cash that doesn’t keep up with inflation means losing purchasing power—that’s suboptimal,” he says. “Why would you leave that [income] on the table? Every part of the portfolio should be contributing to return.”

That philosophy aligns with a broader shift in advisor behaviour. “Advisors are scrutinizing their cash instruments more closely now,” he adds. “They’re demanding the same level of due diligence they would apply to any other part of the portfolio.’ It’s part of the total return equation.”

And the data supports his enthusiasm. The fund’s net asset value has been steadily climbing, supported by consistent monthly distributions—a sign of both underlying stability and active income generation.

“You’re getting the best of both worlds,” Daillie observes. “Regular payouts, and a real return on your liquid assets.”

Calder agrees: “It’s a simple idea that takes a lot of work behind the scenes. But the outcome speaks for itself.”

Why It Matters

Beyond the portfolio math lies a broader behavioural truth: investors often underestimate the strategic role of cash. “We tend to think of cash as inert,” Calder says. “But it’s actually the foundation—the stability layer everything else rests on. You want that layer to be as productive as possible.” And accessible, when opportunity strikes.

For advisors, this reframing has major implications. FHIS isn’t just a placeholder—it’s an upgrade. It helps advisors keep client capital engaged, pursuing a positive real return while maintaining flexibility for future opportunities.

In an environment defined by uncertainty—economic, political, and market-related—that balance of safety and productivity may be the ultimate competitive advantage.

From Passive Cash to Active Opportunity

Calder reflects on the changing perception of fixed income. “Fixed income used to be considered boring,” he laughs. “But the reality is, it’s where a lot of the [market’s] brainpower lives. The opportunities are dynamic, the pace is fast, and active management makes all the difference.”

In a market still searching for equilibrium between risk and restraint, the Franklin Canadian Ultra-Short Bond Fund (FHIS) stands out as a versatile tool for both. It pursues a real return, and a strategic fixed income anchor that tempers volatility without compromising liquidity.

For advisors and investors navigating the “in-between” phase—waiting for clarity on rates, valuations, or market direction—Calder’s message is clear:

“Every part of your portfolio should be working. Your liquid assets don’t have to sit idle. With the right strategy, they can remain accessible while earning a meaningful return.

What's the investor experience been like in the ultra-short bond strategy?

Why the ultra-short strategy makes sense in this period of rates uncertainty?

Every basis point counts. Liquid assets should be made as productive as possible.

Key Takeaways

As markets shift, advisors need to adapt their tools and strategies. Here are the main insights from the discussion:

- Cash Is No Longer Passive - In today’s “higher for longer” environment, excess cash is a silent performance drag. Calder emphasizes that cash should be treated as an active, strategic asset—not idle capital.

- Ultra-Short Bonds Fill the Gap - The Franklin Canadian Ultra-Short Bond Fund (FHIS) bridges the gap between money markets and short-term bonds, offering meaningful yield potential while maintaining liquidity and low volatility.

- Active Management Adds Value - Calder’s team leverages Franklin Templeton’s institutional scale and in-house credit research to identify opportunities early and optimize yield—advantages unavailable in passive or retail cash vehicles.

- Adaptability Across Rate Cycles - FHIS has shown resilience whether rates rise or fall, due to its focus on the “front end of the curve.” It’s designed to capture returns without exposing investors to large rate swings.

- A Strategic Tool for Portfolios in Transition - Advisors can use FHIS to reduce cash drag, manage de-risking phases, or park assets between equity and longer-term bond allocations—keeping client portfolios productive, flexible, and ready for opportunity.

Brian Calder

Portfolio Manager, Senior Bond Trader

Brian Calder is a vice president, portfolio manager and senior trader for Franklin Templeton Fixed Income. Mr. Calder is responsible for co-leading management of Franklin Canadian Government Bond Fund, Franklin Canadian Bond Fund, Franklin Canadian Balanced Fund, Franklin Canadian Ultra Short-Term Bond, and the Franklin Canadian Fixed Income and Balanced SMA strategies. In addition, Mr. Calder is also responsible for the management of a number of institutional accounts. He also performs analysis on federal, provincial and municipal issuers, and is the lead trader for the Franklin Templeton Canadian Fixed Income team.

Mr. Calder joined Franklin Templeton in 2001 and has over 24 years of experience in the financial services industry. Prior to Franklin Templeton, Mr. Calder held a client facing role with another Canadian asset manager.

Mr. Calder holds a degree in Economics from the University of Calgary and also the Chartered Investment Manager (CIM) designation.

About Franklin Templeton Investments

Franklin Resources, Inc. [NYSE:BEN] is a global investment management organization with subsidiaries operating as Franklin Templeton and serving clients in over 150 countries. In Canada, the company's subsidiary is Franklin Templeton Investments Corp., which operates as Franklin Templeton Canada. In Canada, Franklin Fixed Income is a business name used by Franklin Templeton Investments Corp. Franklin Templeton's mission is to help clients achieve better outcomes through investment management expertise, wealth management and technology solutions. Through its specialist investment managers, the company offers specialization on a global scale, bringing extensive capabilities in fixed income, equity, alternatives and multi-asset solutions. With more than 1,400 investment professionals, and offices in major financial markets around the world, the California-based company has over 75 years of investment experience and approximately US$1.6 trillion (approximately CAN$2.2 trillion) in assets under management as of July 31, 2025. For more information, please visit franklintempleton.ca.

Important legal information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell, or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The views expressed are those of the investment manager, and the comments, opinions, and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region, or market. Commissions, trailing commissions, management fees, brokerage fees, and expenses may be associated with investments in mutual funds and ETFs. Please read the prospectus and fund fact/ETF facts document before investing. Mutual funds and ETFs are not guaranteed. Their values change frequently. Past performance may not be repeated. Franklin Templeton Canada is a business name used by Franklin Templeton Investments Corp.

Copyright © AdvisorAnalyst.com, Franklin Templeton Investments

Photo credit: Adobe Stock